EU e-invoicing Practical Guide for Compliance Officers

EU E-Invoicing Standards Explained: A Practical Guide for Compliance Officers

Estimated reading time: approximately 12 minutes

- EN16931 is the European core standard enabling machine-readable, cross-border e-invoicing and automated processing. For 2025-specific rules, read our guide to cross-border e-invoice rules.

- Three compliance levels (Document, Implementation, Specification) define sender, receiver and CIUS obligations for interoperability.

- UBL 2.1 and UN/CEFACT CII are the XML syntaxes used to transmit the standardized invoice data across member states.

- National adaptations such as XRechnung, Factur‑X, and SDI extend EN16931 with country-specific rules and transmission methods.

- ViDA and digital tax reforms are accelerating mandatory EN16931 adoption and moving EU markets toward real-time reporting and CTC models.

Table of contents

- Understanding the EN16931 Framework

- The Three Levels of EN16931 Compliance

- National Implementations Across Europe

- Technical Formats and Data Structures

- Operational Benefits and Business Value

- Compliance Risks and How to Avoid Them

- The ViDA Initiative and Future Developments

- Practical Implementation for Multi-Market Operations

- Frequently Asked Questions

Understanding the EN16931 Framework

EN16931 is the core European standard for e-invoicing created by the European Committee for Standardization (CEN). It provides a unified approach to invoice data exchange across member states and solves the fragmentation that previously required separate templates for each country.

Before EN16931, compliance officers often described the situation as "invoice chaos": multiple templates, different required fields, and heavy manual effort. The standard defines the exact information an invoice must contain — invoice numbers, dates, seller and buyer details (including VAT IDs), item descriptions, VAT rates and amounts, and payment terms — and, crucially, specifies their semantic meaning.

"Semantic consistency is what enables automatic processing across borders — a 'delivery date' means the same thing in Portugal and Poland."

For compliance officers, implementing EN16931 reduces manual processing, decreases errors, and speeds payment cycles once systems are updated to produce semantically correct invoice data.

The Three Levels of EN16931 Compliance

The EN16931 compliance model is three-tiered and clarifies the responsibilities of senders, receivers, and national CIUS implementers:

- Invoice Document Level: The created invoice must include all mandatory fields from the CORE model or the applicable CIUS — structured correctly with accurate calculations and allowed values.

- Implementation Level: Any entity claiming EN16931 compliance must accept and process invoices that conform to the CORE; this prevents receivers from arbitrarily rejecting compliant invoices.

- Specification Level: CIUS specifications must be proper subsets of the CORE and cannot violate CORE rules, assuring compatibility (for example, XRechnung remains compatible with EN16931 while adding German-specific fields).

Compliance officers must verify systems across all three levels: generate compliant invoices, ensure receiving systems accept CORE-conformant invoices, and understand any CIUS constraints relevant to a transaction.

National Implementations Across Europe

EN16931 provides the foundation, but member states add country-specific implementations that introduce additional mandatory fields, identifiers, or transmission routes. Key examples:

- Germany: XRechnung (B2G e-invoice requirements mandatory since 2020; B2B mandatory from 2025) and ZUGFeRD for broader commercial use. XRechnung requires pure XML — standard PDFs no longer qualify.

- France: Factur‑X embeds XML inside a PDF visual representation so humans can view invoices while machines extract structured data.

- Italy: The Sistema di Interscambio (SDI) is a centralized platform through which B2G and B2B invoices are processed.

- Spain: Facturae is used for public administration invoices and plans exist to expand mandatory B2B e-invoicing.

Although national formats vary, they build on EN16931 so the core data elements remain consistent; adapting systems to national differences is easier once the EN16931 data model is generated correctly.

Technical Formats and Data Structures

EN16931 defines a semantic model (EN 16931-1) that sits above two practical XML syntaxes used for exchange:

- UBL 2.1: Verbose, hierarchical, widely adopted in northern Europe and suitable for broad business document needs.

- UN/CEFACT CII: More compact, popular in central Europe; CII is often used as the underlying syntax for German XRechnung deployments.

Key technical point: the semantic model is independent of syntax. Your e-invoicing solution must generate valid XML in either UBL or CII and validate invoices against the official EN16931 schema before transmission. Learn how to validate EN 16931 compliance before you send.

Practical advice: verify your solution supports both syntaxes, performs schema validation, and can convert or route formats according to recipient requirements to avoid rejections.

Operational Benefits and Business Value

EN16931 compliance delivers measurable operational gains:

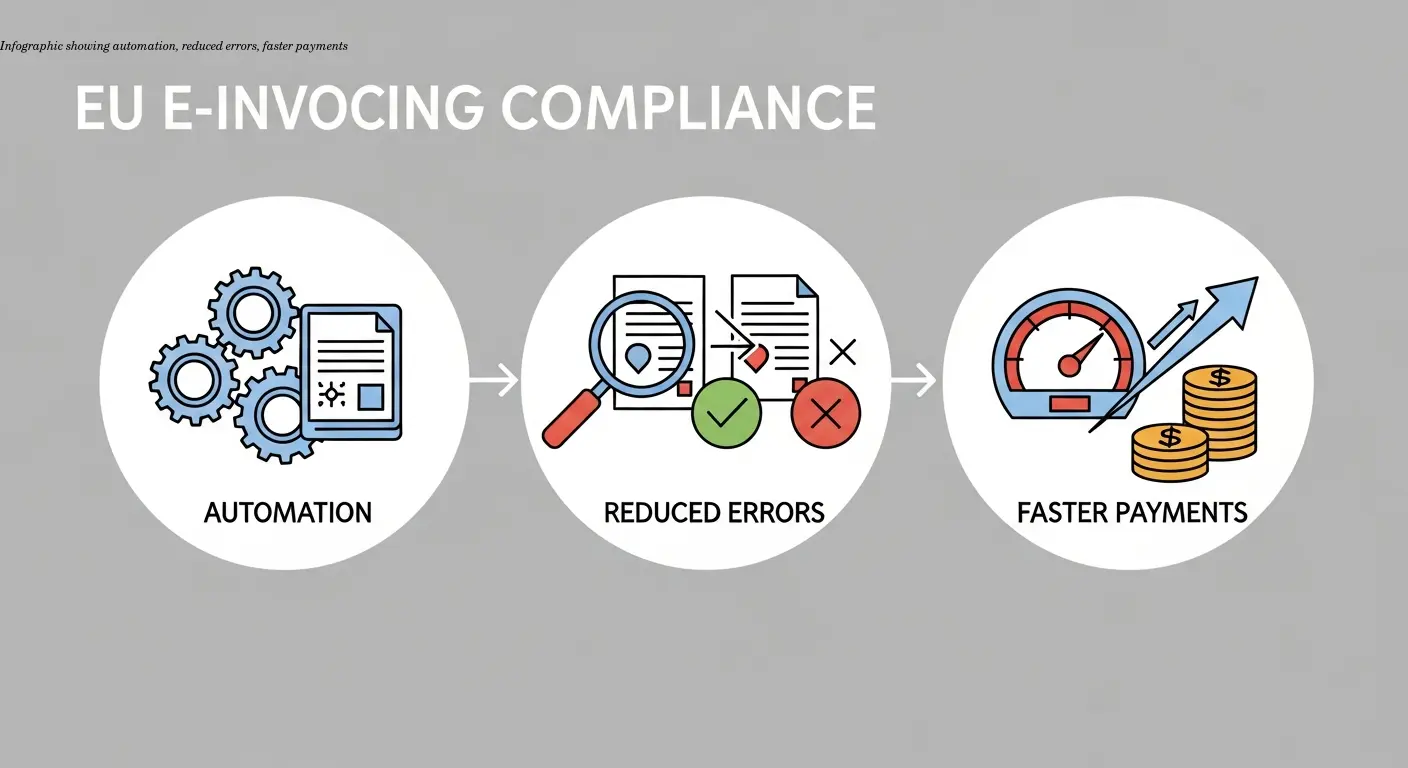

- Automation: eliminates manual data entry — accounts payable teams can drastically reduce per-invoice processing time.

- Cross-border interoperability: a single workflow can process invoices from multiple EU markets without format-specific handling.

- Lower error rates: structured data and validation rules reduce transposition and coding errors.

- Faster payment cycles: speedier verification and approval lead to improved cash flow and easier capture of early-payment discounts.

- Improved VAT handling: structured tax fields support automated VAT reporting and consistency in cross-border transactions.

Although implementation requires investment, the ongoing operational efficiency gains typically justify the effort within a short timeframe.

Compliance Risks and How to Avoid Them

Non-compliance risks:

- Denial of tax deductions: tax authorities may refuse VAT input deductions for non-compliant invoices, creating financial and commercial disputes.

- Invoice rejections and payment delays: missing details or wrong formats can trigger automatic rejections by public sector and other recipient systems.

- Liability and audit risks: posting non-compliant invoices can expose organizations to penalties and corrective requirements during audits.

- Archiving failures: statutory retention (often 10 years) requires audit-proof storage; improper archiving jeopardizes compliance in later audits.

Mitigations: implement automated schema validation before sending, maintain detailed process documentation, conduct periodic audits of generated invoices, train staff, and partner with technology providers who manage evolving standards.

The ViDA Initiative and Future Developments

The EU's Value-added Tax in the Digital Age (ViDA) initiative drives faster adoption of EN16931 to modernize VAT collection and reduce fraud. ViDA promotes structured, near-real-time reporting and continuous transaction controls (CTC).

CEN approved a revised EN16931 version to support ViDA reporting requirements, encompassing B2B scenarios as well as B2G. Mandatory EN16931 adoption is expanding: Germany enforces it for B2B from 2025, and several other member states are following suit.

Recommendation: adopt a phased implementation prioritizing high-volume partners and near-term compliance deadlines to spread effort and learn from early pilots.

Practical Implementation for Multi-Market Operations

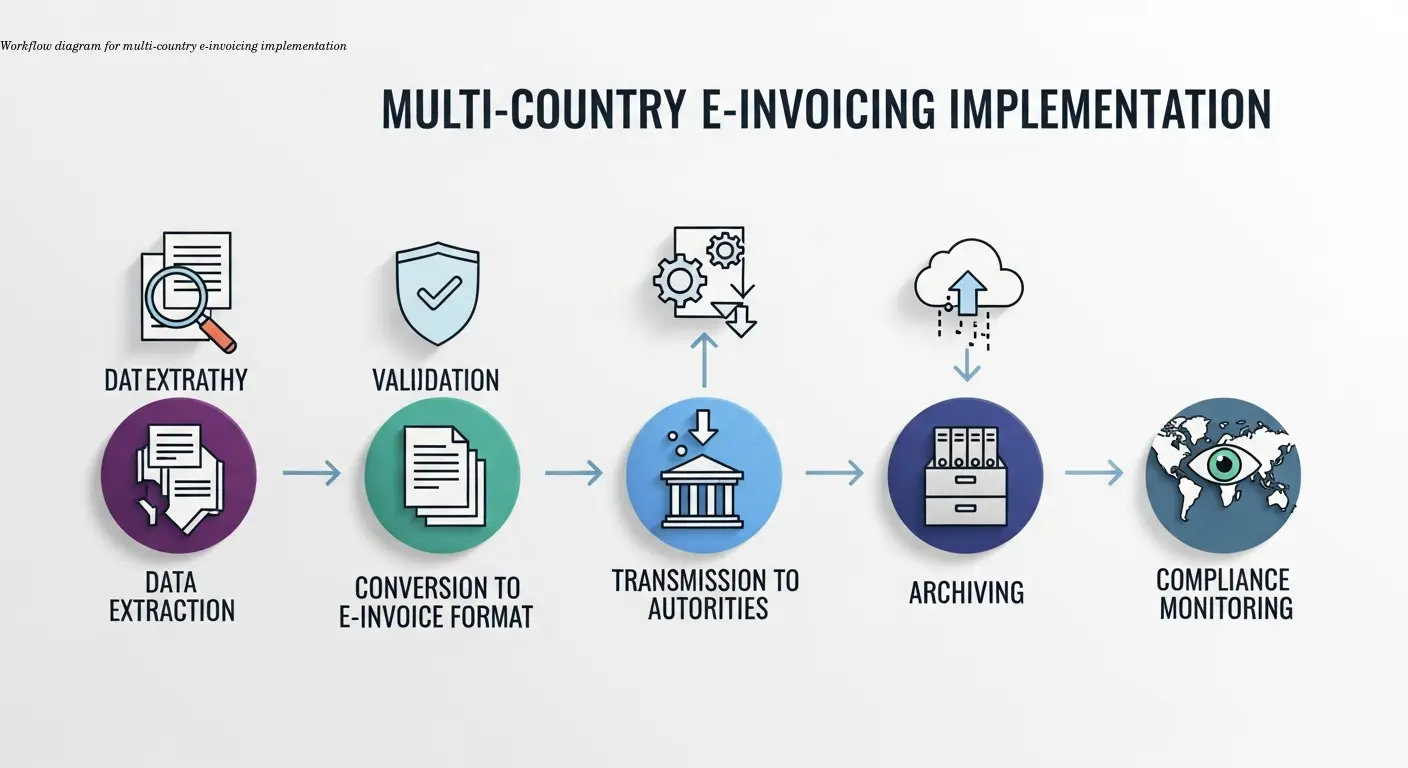

For multi-market appliance retailers and distributors, implementation should be methodical:

- Market assessment: identify countries, transaction volumes, and mandatory requirements to prioritize deployment.

- Choose technology carefully: look for platforms that generate validated XML (UBL/CII), apply CIUS variations, and integrate with ERP systems.

- Test with partners: real-world pilot transactions reveal integration issues that schema validation alone misses.

- Document and archive: keep process documentation, compliant invoice samples, and audit-proof archiving in place.

- Plan maintenance: assign responsibility for monitoring EN16931, CIUS updates, and ViDA developments; update systems proactively.

Think of e-invoice creation as part of product localization — like translating manuals — and invest in tools and partners that streamline the process across markets. Our guide shows how to create e-invoices for EU compliance step by step.

Frequently Asked Questions

What exactly is EN16931?

EN16931 is the European standard for electronic invoicing established by the European Committee for Standardization. It defines a core data model specifying what information invoices must contain and two XML syntaxes (UBL 2.1 and UN/CEFACT CII) for implementing that model. The standard ensures invoices can be exchanged and processed automatically across EU member states.

Do I need to comply with EN16931 for all my EU invoices?

Requirements vary by country and transaction type. Public sector invoices (B2G) across the EU generally require EN16931 compliance already. For B2B transactions, compliance is becoming mandatory in more countries - Germany requires it from 2025, with other member states following similar timelines. Even where not yet mandatory, EN16931 compliance offers operational benefits.

Can I still send PDF invoices?

In many EU countries, standard PDF invoices no longer qualify as valid e-invoices because they're not machine-readable. Germany explicitly requires structured XML formats for e-invoices. Some countries accept hybrid formats like ZUGFeRD or Factur-X that combine PDF visualization with embedded XML data, but pure PDF invoices are being phased out.

What's the difference between EN16931 and XRechnung?

EN16931 is the EU-wide standard. XRechnung is Germany's national implementation - a Country-specific Implementation Specification (CIUS) that builds on EN16931 while adding German-specific requirements like the Leitweg-ID for routing invoices to public authorities. All XRechnung invoices are EN16931-compliant, but not all EN16931 invoices meet XRechnung's additional requirements.

What happens if my invoice doesn't comply?

Non-compliant invoices face several risks: automatic rejection by recipient systems, payment delays, denial of VAT input tax deductions by tax authorities, and potential penalties during audits. Public sector buyers will typically reject non-compliant invoices automatically, requiring resubmission and delaying payment.

How do I validate my invoices are EN16931 compliant?

Validation tools check invoices against the official EN16931 schema to verify they contain required elements in proper structure. Many e-invoicing solutions include built-in validation. Independent validators are also available online. Validation should occur before sending invoices to catch errors early.

Do I need different systems for each EU country?

Not necessarily. While national implementations add country-specific requirements, they all build on the EN16931 foundation. A properly designed system can generate the core EN16931 data model and then apply country-specific variations as needed. This is more efficient than maintaining completely separate systems for each market.

How does EN16931 compliance affect my archiving requirements?

E-invoices must be stored in compliance with statutory retention requirements (often 10 years) in an audit-proof manner. The invoices must remain readable and verifiable throughout the retention period. Some countries have specific requirements about archiving format and location. Your archiving solution should maintain invoice integrity and support retrieval for audit purposes.

Related articles

Create e-invoice for EU Compliance - Practical SME Guide

Learn how to create e-invoice compliant with EN 16931 and EU rules. Practical steps for SMEs to validate, sign, archive (10 years) and choose the right tools.

Cross-Border E-Invoice Compliance for 2025 Businesses

Cross-border e-invoice compliance in 2025: EN 16931, Germany B2B rules, ViDA reporting. Get practical steps and AI automation expertise to speed implementation.

Practical e-invoice validator Guide for Compliance Teams

Ensure EN 16931 compliance with an e-invoice validator—structural, semantic and calculation checks. Tips for compliance teams; AI automation expertise.

Practical b2g e-invoice creation for EU Government Suppliers

Learn practical b2g e-invoice creation to automate XRechnung submission, speed payments and ensure compliance - by AI automation experts for EU suppliers.

About the author

Alexander Lutsyuk · Founder & Operator

Alexander Lutsyuk is the founder of Algoran and runs E-Rechn.de. He has worked for years in automation, digital content and SEO, currently as an on-page SEO adviser at SEO-Küche Internet Marketing GmbH & Co. KG. With E-Rechn.de he combines hands-on automation expertise with the practical demands of the EU e-invoicing mandate: XRechnung, ZUGFeRD, Factur-X and EN 16931. He holds an M.Sc. from Humboldt University of Berlin and is a BVDW-certified specialist.

Education: Humboldt-Universität zu Berlin

BVDW-certified specialist